The concept of guaranteed loan approval can be interesting, particularly for individuals looking for financial assistance with less-than-perfect credit scores. However, it is important to understand that on the planet of lending, the idea of assured approval could not always align with actuality. In this article, we’ll delve into the complexities of assured mortgage approval in Canada, providing insights into what borrowers ought to know and contemplate.

The Reality of Guaranteed Approval

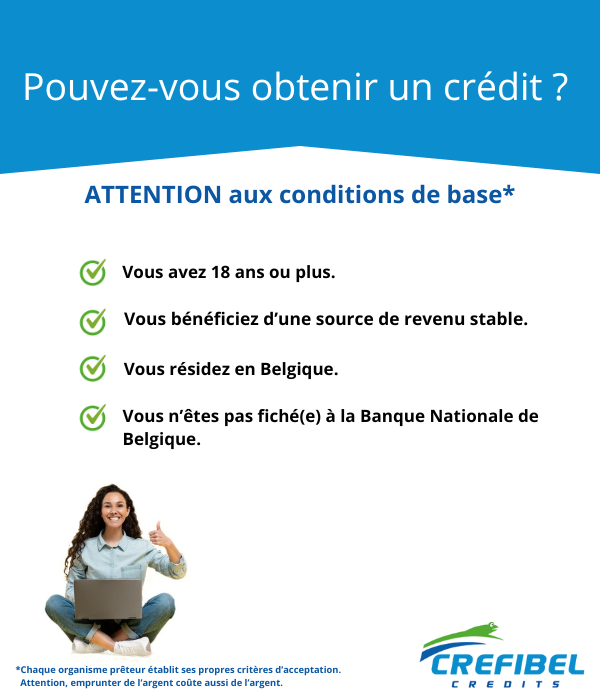

While some lenders could promote assured mortgage approval, it’s essential to method such claims with caution. In Canada, respected lenders consider various elements when evaluating mortgage applications, together with credit score history, revenue, debt-to-income ratio, and more. No lender can genuinely guarantee approval for each applicant with out assessing these elements.

Benefits of Reputable Lenders

When in search of a mortgage, it’s necessary to focus on reputable lenders that prioritize responsible lending practices. Reputable lenders think about the borrower’s financial situation and creditworthiness before approving a loan. While approval is not guaranteed, Comment Obtenir Un Micro PrêT Aucun Refus borrowers can benefit from a more transparent and honest analysis process.

Considerations for Borrowers

High-Interest Rates

Lenders that advertise guaranteed approval could offset the danger by charging greater interest rates. Borrowers ought to be cautious of loans with exceptionally excessive rates of interest, as they can lead to substantial reimbursement amounts.

Predatory Lending

Some lenders that promise assured approval could engage in predatory lending practices. Borrowers ought to be careful for lenders that strain them into taking loans with unfavorable terms or hidden fees.

Credit Checks

Even lenders offering assured approval typically perform credit checks to assess the borrower’s credit history. While the credit rating may not be the sole figuring out factor, it nonetheless performs a task within the decision-making process.

Alternatives to Guaranteed Approval

Instead of focusing on guaranteed approval, debtors should discover alternate options to improve their possibilities of acquiring a mortgage:

- Improve Credit Score: Work on enhancing your credit score rating by paying bills on time, lowering outstanding debt, and correcting any errors in your credit report.

- Seek Co-Signer: Having a co-signer with good credit score can strengthen your mortgage application and improve your probabilities of approval.

3. Steady Income: Demonstrating a gentle source of income can increase your eligibility for loans. Lenders typically contemplate your capacity to repay the loan.

four. Collateral: Some lenders supply secured loans the place you provide collateral, corresponding to a vehicle or property, to secure the mortgage. This can increase your chances of approval.

- Responsible Borrowing: Only borrow what you can afford to repay. Lenders are extra likely to approve loans for people with accountable borrowing habits.

Navigating the Lending Landscape

- Research Lenders: Research respected lenders in Canada that prioritize accountable lending practices.

- Check Eligibility Criteria: Review the eligibility standards for every lender to determine if you meet their necessities.

three. Gather Documentation: Prepare the required documentation, together with proof of id, earnings, and credit score history.

4. Complete Application: Fill out the appliance precisely and provide all required info.

- Review Terms: If approved, rigorously evaluation the loan terms, including interest rates, charges, and repayment schedule.

- Choose Reputable Lender: Opt for lenders that focus on evaluating your financial state of affairs somewhat than guaranteeing approval.

Conclusion

While guaranteed mortgage approval may be a tempting concept, debtors ought to method it with warning and think about the reality of responsible lending practices. Reputable lenders prioritize assessing borrowers’ financial situations and creditworthiness to make knowledgeable selections. Instead of solely focusing on assured approval, borrowers ought to concentrate on enhancing their monetary standing and exploring alternate options that improve their chances of acquiring a mortgage.